Main market themes

Global equity markets extended the rally on Thursday on the back of optimism of trade deal despite mixed US data. US Treasury Secretary Steven Mnuchin said the phase one trade deal will be signed at the beginning of January as the deal was completely finished. US initial weekly jobless claims fell by 18K to 234K although continuing claims rose from 1.667 million to 1.722 million.

Manufacturing sector remained weak with the Philadelphia Fed Business index slipped to 0.3 from 10.4. Housing data also disappointed with the existing home sales fell by 1.7% mom missing market expectations.

Markets will watch out for 3Q US GDP data, PCE income and spending data and University of Michigan business sentiment data later today.

The Bank of Japan kept its benchmark interest rate unchanged as widely expected. The BoJ Governor Kuroda was more upbeat on growth outlook saying that global outlook has brightened somewhat due to preliminary USChina trade deal. However, he also countered the view that monetary policy has reached its limit saying that deepening negative rates were among the policy option. His view was echoed by the new research study by ECB staff. The research paper said the lower overnight rate is associated with stronger loan growth and the negative rates could even go lower further before any cuts become counterproductive amid a severe shock to growth.

BOE left bank rate steady, still cautious ahead of Jan 2020 Brexit headline: The Bank of England MPC voted 7-2 (unchanged) to keep bank rate steady at 0.75% as widely expected and reiterated its hawkish stance. Among key points being of the latest statement include that BOE expects growth to pick up from current below-potential rates, “supported by the reduction of Brexit-related uncertainties, an easing of fiscal policy and a modest recovery in global growth”. Economic data were broadly in line with November Inflation Report, global growth offers signs of stabilising. The partial de-escalation of US-China trade war provides additional support to outlook but trade tensions remain elevated. BOE said that U.K. GDP is expected to grow marginally in 4Q and financial markets remained sensitive to domestic policy development. There are signs that the labour market is loosening, although it remains tight. Pay growth “has eased somewhat” but unit labour costs continued to grow at rates consistent to meet its 2% inflation in the medium term. CPI is still expected to fall to 1.25% by spring. BOE appeared to remain cautious in its latest statement, sticking to its “wait and see approach” ahead of key Jan 2020 Brexit deadline. It repeated that at this juncture, monetary policy could still respond in either direction and it will continue to monitor closely the responses of companies and households to Brexit developments as well as the prospects for a recovery in global growth. It reinforced its hawkish stance that “some modest tightening of policy, at a gradual pace and to a limited extent, may be needed to maintain inflation sustainably at the target”, barring from the materialisations of Brexit and global growth risks

Today’s Options Expiries for 10AM New York Cut (notable size in bold)

- EURUSD: 1.1020 (EUR610mn); 1.1025 (EUR696mn); 1.1130 (EUR725mn); 1.1140 (EUR532mn); 1.1145 (EUR624mn); 1.1150 (EUR2.7bn); 1.1180 (EUR519mn); 1.1200 (EUR581mn); 1.1225 (EUR401mn); 1.1250 (EUR1.4bn)

- USDJPY: 108.00 (USD804mn); 109.00 (USD577mn); 109.10 (USD385mn); 109.25 (USD668mn); 109.45 (USD416mn); 109.50 (USD2.8bn); 109.70 (USD429mn); 110.00 (USD1.6bn); 110.50 (USD1.1bn)

- GBPUSD: 1.2905 (GBP424mn); 1.2950 (GBP293mn); 1.2980 (GBP371mn); 1.3000 (GBP692mn); 1.3016 (GBP384mn); 1.3040 (GBP506mn); 1.3050 (GBP382mn)

- AUDUSD: 0.6805 (AUD306mn); 0.6820 (AUD254mn); 0.6825 (AUD605mn); 0.6850 (AUD542mn); 0.6870 (AUD306mn); 0.6950 (AUD223mn)

EURUSD (Intraday bias: Neutral Bullish above 1.1100 Bearish below)

From a technical and trading perspective, Caution is counseled as we note that price failed to close above the monthly R1, the repeated failure to take out that level on a closing basis today would likely concern newly minted longs, however as 1.1110/00 now acts as support their is a window for another drive higher to target the equidistant swing objective sited at 1.1250, 1,1160 is the key upside hurdle ahead of Friday’s highs.. A close sub 1.1110 would suggest a false topside break and reset sites on another test of bids towards 1.1060 NO CHANGE IN VIEW

GBPUSD (Intraday bias: Bearish target 1.30 achieved)

From a technical and trading perspective, anticipated failure below 1.33 has initiated a deeper correction to the 1.30 break point. On the day look for 1.32 to act as resistance, only a daily close back above 1.3250 would alleviate downside pressure, setting a base to revisit 1.34

GBPUSD…UPDATE a failure to recapture 1.3130 today will be a further bearish development opening a test of trendline support down to 1.28

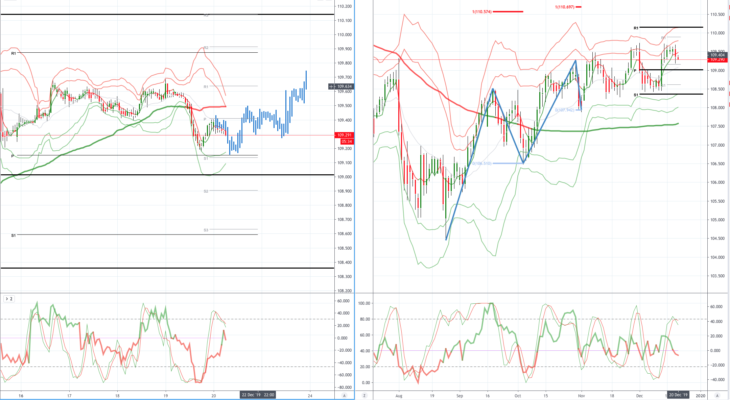

USDJPY (intraday bias: Bullish above 109.10 targeting 110.50)

From a technical and trading perspective, the close through 109.30 would suggest downside failure and reset sites on 110. As 109.10 acts as support look for a test of the equidistant swing objective at 110.50, however a close below 109 would suggest another headfake to the topside and return to bids towards 108.50. NO CHANGE IN VIEW

AUDUSD (Intraday bias: Bullish above .6850 targeting .7000)

From a technical and trading perspective, as .6850 caps corrections look for further upside pressure targeting a retest of October highs. Test of October offers underway as these are eroded look for a test of offers and stops to 0.7000. Caution as Friday printed a key reversal day, however, we failed to flip the daily chart bearish as per the near term Volume Weighted Average Price, follow through selling today will do so and would be of significant concern to the bullish bias.

AUDUSD…UPDATE Daily chart has flipped bearish, .6850 bids being eroded, bulls trying to defend .6840 a further failure here opens a move to test bids back towards .6800 NO CHANGE IN VIEW

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.