Main market themes

- The coronavirus remains the primary focus at present for the market. The number of people infected with the virus continues to rise sharply, with the total number of cases in China now exceeding those during the SARS epidemic, although the mortality rate is significantly lower at this stage than SARS (around 2% compared to SARS at 9.6%). The WHO has called an emergency meeting to decide whether to declare it a global emergency.

- The potential economic fall-out from the virus is also becoming more visible with BA and Lufthansa cancelling flights to and from China and Toyota saying it would stop all production in China until February 9th. There is the potential for disruptions to global supply chains if there are more widespread and extended production shutdowns.

- Markets had initially gotten a boost from Apple, Boeing and General Electric following their upbeat 4Q earnings but lost steam towards the end of the session after Powell mentioned the uncertainties over outlook posed by the novel Coronavirus outbreak. Futures markets point to further losses of around 0.5% as Asian markets have posted losses overnight .

- Risk aversion prompted traders to buy treasuries, pushing yields lower by 5-7bps. Gold was flat, crude oils ended mixed. Brent crude picked up 0.5% to $59.81/barrel.

- Fed kept rate steady; stressed the need to return inflation to 2% target: The Federal Reserve kept fed funds rate target range unchanged at 1.5-1.75% as widely expected on Wednesday, offering no surprise in a barely changed monetary policy statement. However, policy makers did make a slight change to the statement that says the current stance of monetary policy is appropriate to support inflation “ returning to” its symmetric 2% target. In the post-meeting press conference. Fed Chair Jerome Powell said that the change was made to send a clear signal that the committee was not comfortable with inflation running persistently below 2% target. Powell mentioned that trade policy uncertainty remained elevated, and the Fed is carefully monitoring the situation of the Coronavirus outbreak which is still in its early stage but could pose uncertainty to economic outlook. He mentioned that it is a bit surprising that sustained levels of historically low unemployment rate hasn’t been able to push up wages. He said that the labour market continues to perform well with strong job creation, low unemployment and labour force participation continuing to move up.

- US advanced good trades widened in December: Preliminary report shows that goods trade deficit widened to $68.3b in December (Nov: -$63.0b revised) as imports of goods rebounded to increase 2.9% MOM (Nov: -1.3%) while exports pulled back to a softer 0.3% MOM growth (Nov: +0.8%). In the similar report, December wholesale inventory remained lacklustre, recording a 0.1% MOM decline (Nov: +0.1%) while retail inventory was flat (Nov: -0.8%).

- US pending home sales plunged at year end: US pending home sales plunged by 4.9% MOM in December (Nov: +1.2%), its largest drop in more than nine years. The index tracks contract signings to purchase previously owned homes in the US and the unexpected slump at the last month of 2019 suggests that lean inventory continued to limit sales in what appears to be a strengthening market in recent months. On a separate note, mortgage applications rose 7.2% last week (previous: -1.2%), driven by lower interest rates across the board.

- UK house prices jumped as Brexit fear lifted: The Nationwide House Price Index beat estimate to record 0.5% MOM increase in January (Dec: +0.1%), leaving the annual growth at 1.9% YOY (Dec: +1.4%, its largest gain in more than a year. Prices began to pick up at a faster pace at the end of the year as the Tories’ decisive victory at an early December election significantly lifted Brexit uncertainties that drove buyers back into the housing market.

- Traders now turn focus to the Bank Of England’s policy rate decision today. Markets have pared down their earlier expectations of a rate cut with the money market now pricing in a lower 45.5% chance of a 25bps reduction in Bank Rate. Majority of economists surveyed by Bloomberg are also expecting the central bank to keep its benchmark rate steady at 0.75%.

Today’s Options Expiries for 10AM New York Cut (notable size in bold)

- EURUSD: 1.0890 (EUR401mn); 1.0900 (EUR459mn); 1.0985 (EUR1.3bn); 1.1000 (EUR1.1bn); 1.1005 (EUR355mn); 1.1045 (EUR623mn); 1.1150 (EUR369mn)

- GBPUSD: 1.2975 (GBP350mn); 1.3100 (GBP585mn); 1.3135 (GBP270mn)

- USDJPY: 109.00 (USD547mn); 110.00 (USD402mn); 110.50 (USD657mn)

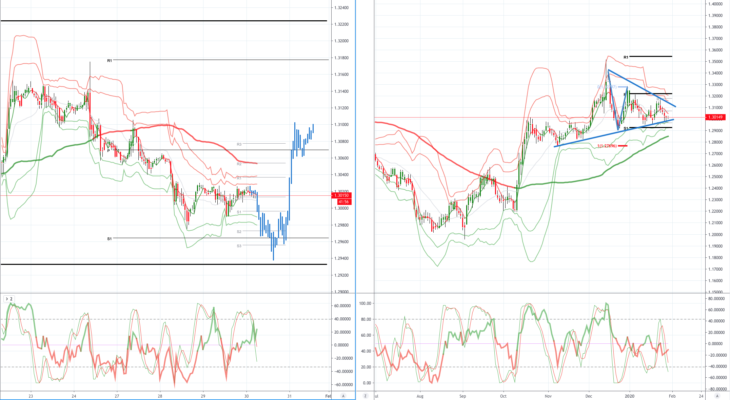

EURUSD (Intraday bias: Bearish below 1.1040)

From a technical and trading perspective, A daily close today back through 1.1050 could prompt further short covering into the end of the month. Citi FX quants asset rebalancing signal is strong and points at USD selling against JPY and EUR at month end. Note a closing breach of 1.0980 would suggest further sustained downside risk exposing bids and stops below 1.09.

GBPUSD (Intraday bias: Bearish below 1.3065)

From a technical and trading perspective, expect further consolidation with a mild downside bias ahead of today’s knife edge rate decision. As bids below 1.2950 stem downside probes, there is likely further scope for upside if the BOE that follows the FED’s lead, holding rates steady, this would prompt rapid short covering post the release. A daily close above 1.3075 would flip the daily charts bullish and would like be the catalyst for further short covering/profit taking into month end.

USDJPY (intraday bias: Bearish below 109.60)

From a technical and trading perspective, as anticipated sentiment and momentum divergence has been addressed with the breach of 109.80/60 as this levels caps upside attempts now look for a move to test bids at 108.60 and stops below. On the day only a close back above 109.60 would delay downside objectives.

AUDUSD (Intraday bias: Bearish below .6820)

From a technical and trading perspective, the overnight gap through the ascending trendline support suggests the potential for further downside to test equidistant swing support sited towards .6750. As .6730 survives there is a window to set a base, however, a failure here will open a test of bids back to .6700 and stops below.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.